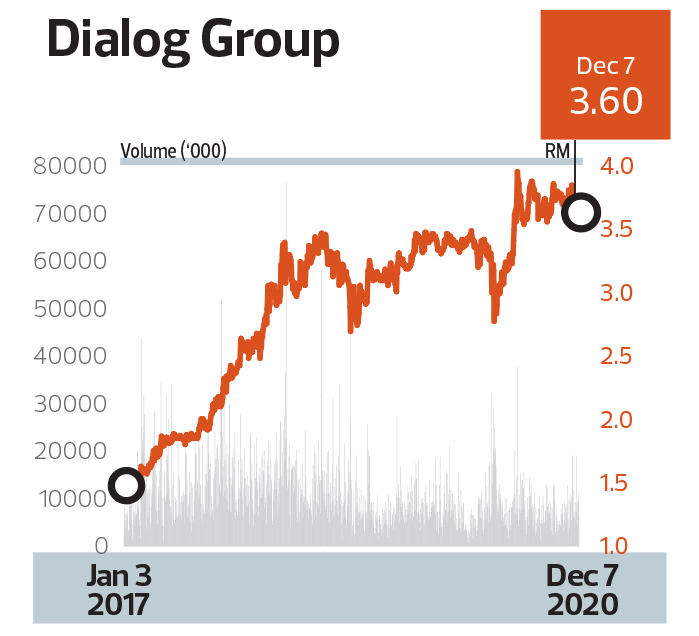

Almost all oil and gas equity analysts view Dialog Group Bhd in a positive light. And the optimism is understandable, considering that it has grown from a company with a market capitalisation of RM55 million at the time of its floatation exercise in 1996, to its current level exceeding RM20 billion.

The catalyst for growth at Dialog came after it forked out RM700 million to build, own and operate its tank terminals facility in Tanjung Langsat, Johor, in 2007. From there, in 2009, Dialog moved on to develop Pengerang Deepwater Terminals, which commenced operations in 2015.

In a nutshell, the group’s terminals serve as tank facilities for the handling, storage, blending and distribution of petroleum products for oil majors and traders.

Tanjung Langsat has three terminals with a capacity of around 765,000 cubic metres (cbm), with the total volume likely to reach one million cbm.

Pengerang Deepwater Terminals, meanwhile, spans 1,200 acres and has two operating jetties with an additional three in the pipeline. It is making a mark with its 24m deep berths, enabling it to handle the largest of vessels — be they very large crude carriers (VLCC), ultra large crude carriers (ULCC) and liquefied natural gas (LNG) vessels up to Q-Max size, which are about 350m in length.

The second phase of this development — Pengerang Terminals (Two) Sdn Bhd — is a dedicated industrial terminal with about two million cbm in storage capacity for crude, refined petroleum and petrochemical products. Equipped with a deepwater jetty facility, it also has LNG regasification facilities and storage tanks, among others.

Dialog also roped in the right partners to help with some of the infrastructure. Pengerang Independent Terminals Sdn Bhd, for instance, is a joint venture between Dialog, which has a 46% stake, Royal Vopak with 44%, and the Johor state government with the remaining 10%. Vopak is a huge independent provider of storage facilities for bulk liquids and gases.

With its tank terminal business, Dialog has transformed into a major oil and gas player, with strong earnings and good prospects.

For its first quarter ended September 2020, the company registered a net profit of RM146.62 million from RM331.66 million in sales. In contrast to the corresponding period a year ago, net profit declined by 10.94% while revenue tumbled 48.64%.

Dialog explains that the lower net profit for the first three months of the year was a result of the company booking a RM28.5 million non-cash fair value gain. It adds that for the first quarter of the financial year ended Sept 30, the group achieved a 5.3% increase in its net operating profit after tax of RM148.1 million, against RM140.6 million registered in the corresponding quarter last year.

Dialog attributes the lower revenue to slower downstream activities.

On its prospects, the group is confident that “its business model is well structured to manage and sustain itself through periods of economic uncertainty, oil price volatility and currency movements … Overall, the economic environment is expected to remain extremely challenging in the short to medium term”.

Dialog’s balance sheet strength is also commendable. As at end-September this year, it had cash and cash equivalents of RM1.05 billion, while on the other side of the balance sheet, it had long-term borrowings of RM1.53 billion and short-term debt commitments of RM405.53 million. This works out to net debt of RM885 million and net gearing of 0.2 times.

Meanwhile, its accumulated reserves stood at RM2.59 billion.

From June 2016 to June 2019, Dialog’s stock gained about 120%. Over the past three years from 2016 to 2019, the group has paid out 40% of its net profits as dividends. It paid out 2.65 sen a share in dividends in FY2017, 3.2 sen per share in FY2018 and 3.8 sen per share in FY2019.

Dialog has bagged the award for highest growth in profit after tax over three years, with a risk-weighted three-year profit after tax compound annual growth rate of 22%.